Winter 2026: Designing Credit for a Changing Monetary Order

There’s a widening gap between real estate lending markets and the economic reality owners are living in. Many assets are underwater. Lenders are stuck. Borrowers are frustrated. Liquidity is constrained, interest rates are high, and legacy financing tools are failing to serve either side of the table.

What we’re facing isn’t a cyclical lull—it’s a structural transition.

Renowned hedge fund manager Ray Dalio (Founder, Bridgewater Associates with $100+ billion AUM) has discussed this at length: a long-term debt cycle is concluding, and a new monetary order is emerging. Like it or not, we all get to live through it. For commercial real estate owners still anchored to assumptions from prior cycles, understanding this structural shift is mission critical.

Over the past few editions, I’ve written about the need to rethink treasury strategy (Winter 2024), the role of Bitcoin in long-term portfolio resilience (Summer 2024), and the implications of legacy planning in a world of capital evolution (Summer 2025).

Now, it’s time to take the next step: making the capital stack itself more resilient.

For decades, real estate served not only as a productive asset, but as a primary store of value. A position earned through scarcity, durability, tax efficiency, and institutional trust. We are entering a new monetary era and that dominance is quietly, yet steadily, eroding.

Bitcoin is reshaping the store-of-value conversation and capital has begun to migrate. We are witnessing the slow unwind of real estate’s monetary premium. This is the portion of its valuation driven not by use or income, but by its perceived scarcity and long-term value retention. That premium is moving into Bitcoin.

The question is no longer if but how you position yourself in response.

In Winter 2024, I introduced the concept of treasury strategy: reallocating a percentage of your free cash flow into Bitcoin rather than holding 100% in USD or its equivalents.

That is the first step because it’s simple, controllable and educational.

In practical terms, it preserves purchasing power, enables you to build and maintain adequate reserves for maintenance and CapEx, and enhances creditworthiness. I view it as your “operational defense”. A modern tactic for day-to-day property management in a system where expenses are rising faster than rents.

The next evolution in strategy is understanding and applying dual-collateral loan structures.

The idea of securing a loan with more than just the subject property is nothing new. Lenders have long relied on personal guarantees, UCC filings, or pledged securities. What’s new (and timely) is the use of Bitcoin as that secondary layer of collateral.

This is not a mark-to-market margin loan. It’s a unified capital structure that underwrites both the real estate and the Bitcoin, together, in a long-duration credit facility.

And here’s why it matters:

✔ It’s written over 5, 7, or 10 years—so you’re underwriting a long-term macro trend, not day-to-day volatility. No margin calls. No forced liquidations. No rehypothecation.

✔ Bitcoin becomes additive, liquid collateral that enhances the lender’s downside protection while preserving the borrower’s upside.

✔ Most critically, it acts as a counterbalance. As monetary premium drains from real estate, it can be recaptured through Bitcoin’s appreciation.

Here’s what most people miss: this structure reduces risk over time. As Bitcoin appreciates and the loan amortizes, the collateral ratio improves. Every year, the position gets stronger.

This structure creates something we haven’t seen in decades: predictability, incentive alignment, and compounding strength over time.

The natural question is: why change the existing structure at all? Well, traditional loans concentrate risk at maturity. If cap rates expand, liquidity dries up or tenant preferences change, borrowers are forced into recapitalizations or distressed situations. That pressure shapes behavior long before the maturity date.

When an owner knows the entire strategy depends on a narrow refinance window, decisions become defensive. Tenant selection prioritizes speed over quality. Capital expenditures are deferred and improvements are value-engineered. The investment horizon compresses and corners get cut. Over time, this behavior degrades asset quality across the market.

By contrast, a structure that reduces dependence on the refinance window expands optionality. With a secondary appreciating collateral layer strengthening the balance sheet over time, the owner is no longer forced to optimize for a single liquidity event.

Tenant underwriting becomes more selective. Lease terms can align with long-term objectives rather than short-term stability. Capital improvements can be executed with a multi-cycle mindset instead of a maturity-driven clock. Asset quality improves. Cash flow durability improves. Decision-making improves.

By integrating Bitcoin into the credit stack, borrowers retain ownership of real assets for business use, tax efficiency, and investment continuity while gaining exposure to liquidity, asymmetric upside, and structural optionality.

This matters most to the people this newsletter is built for: entrepreneurs, business owners, operators and landlords. People who don’t just invest in buildings—they use them.

You’re not allocating to real estate just to park cash. You’re solving for function, control, and stability in your core business. We are all busy personally and professionally but that is not an excuse for ignoring what’s happening in the broader macro landscape. The changes taking place have major implications and will impact everyone.

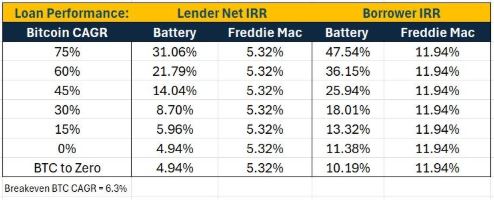

Bitcoin-backed lending is no longer fringe. In March 2025, Newmark Capital refinanced a 63-unit apartment building in Philadelphia using this structure. The building appraised at $16.5 million. Battery Finance provided an $11 million loan (67% LTV), which paid off the existing first lien, funded $250,000 in capital improvements, and included a $1.5 million Bitcoin allocation.

The loan is secured by a first lien on the real estate and a pledge on the Bitcoin. The borrower and lender split the BTC upside 60/40 at maturity in Year 10.

The deal won the CoStar Impact Award for Multifamily Development of the Year in 2025.

Most importantly, the underwriting speaks for itself. Projected returns reflect a 25–35% enhancement in equity margin relative to a conventional structure. In an industry where operators fight for 50 basis points of spread, that magnitude of improvement meaningfully alters risk tolerance, capital allocation, and long-term equity growth.

For lenders, this structure introduces additional high-quality collateral, better aligns incentives and participation in asymmetric upside without sacrificing senior lien protection on the real estate.

That is just the beginning. Institutions like Bank of America, JPMorgan, Citigroup, Wells Fargo, Schwab, Goldman Sachs, BNY Mellon, and PNC have announced new Bitcoin credit platforms launching in 2026. The infrastructure is finally catching up. Regulatory rails are being laid. The Genius Act, Clarity Act, and the Bitcoin Strategic Reserve are accelerating this adoption.

Real estate is no longer the uncontested store of value it once was. Owners must begin thinking in hybrid structures; frameworks that allow them to participate in both the existing system and the emerging one.

This structure doesn’t require you to become a Bitcoin expert. It doesn’t require you to sell your property, abandon your business, or bet the farm. It’s about engaging with new tools that complement and enhance what you already own. Tools that strengthen your position in an environment that is evolving with or without your participation.

More on Topic

Summer 2025: Don’t Leave It To The Kids

Winter 2024: Preserving Your Real Estate Wealth with Bitcoin

Summer 2024: Real Estate Risks & Opportunities in the Age of Bitcoin